Study Notes

Overview

Welcome to your essential guide to Business Objectives for AQA GCSE Business. This topic is a cornerstone of the specification (3.1.2) and a favourite of examiners because it connects to everything else you'll study. Understanding why a business exists and what it's trying to achieve is the first step to analysing its decisions and performance. This guide will break down the different types of objectives, explain how and why they change, and show you how to apply this knowledge to exam questions to secure top marks. We will cover the key financial goals, such as survival and profit, and the increasingly important non-financial goals, like social responsibility and personal satisfaction. By the end of this guide, you will be able to confidently explain the purpose of setting objectives and evaluate their impact on a business's strategy.

Key Concepts: Financial vs. Non-Financial Objectives

Financial Objectives

These are the goals that are directly related to the financial performance of the business. They are typically measurable in monetary terms.

Survival: For a new business, or any business during a crisis (like a recession or the COVID-19 pandemic), survival is the primary objective. The focus is purely on generating enough cash to cover costs and avoid exiting the market. It's a short-term, defensive objective.

Profit: This is the most common objective. It's the surplus left after total costs are deducted from total revenue. However, candidates must be more specific:

- Profit Maximisation: Making as much profit as possible. This is often the main goal for Public Limited Companies (PLCs) to satisfy their shareholders with high dividend payments and a rising share price.

- Profit Satisficing: Making just enough profit to satisfy the owners or key stakeholders. A sole trader might choose this to have a better work-life balance, rather than working all hours to maximise profit.

Sales/Revenue Growth: Increasing the value or volume of sales. This can help a business increase its market presence and brand recognition.

Market Share: This is the proportion of total sales in a market that a business holds. A business might aim to increase its market share to become the market leader, which can give it more power and influence.

Financial Security: Ensuring the business has enough cash to meet its day-to-day expenses and can withstand unexpected events.

Non-Financial Objectives

These goals are not directly linked to the financial performance of the business, but can have a significant impact on long-term success.

Social Objectives: This involves behaving in a way that benefits society. Examples include using sustainable materials, reducing pollution, or donating a percentage of profits to charity. This can improve a business's reputation and attract customers.

Personal Satisfaction: For many entrepreneurs, particularly sole traders, a key objective is to enjoy their work and have control over their own lives. They may be willing to accept a lower profit to achieve this.

Employee Welfare: Looking after the staff. This can include providing good working conditions, training opportunities, and fair pay. This can lead to a more motivated and productive workforce, reducing staff turnover.

Customer Satisfaction: Putting the customer first by providing high-quality products and excellent service. This can lead to repeat business and positive word-of-mouth recommendations.

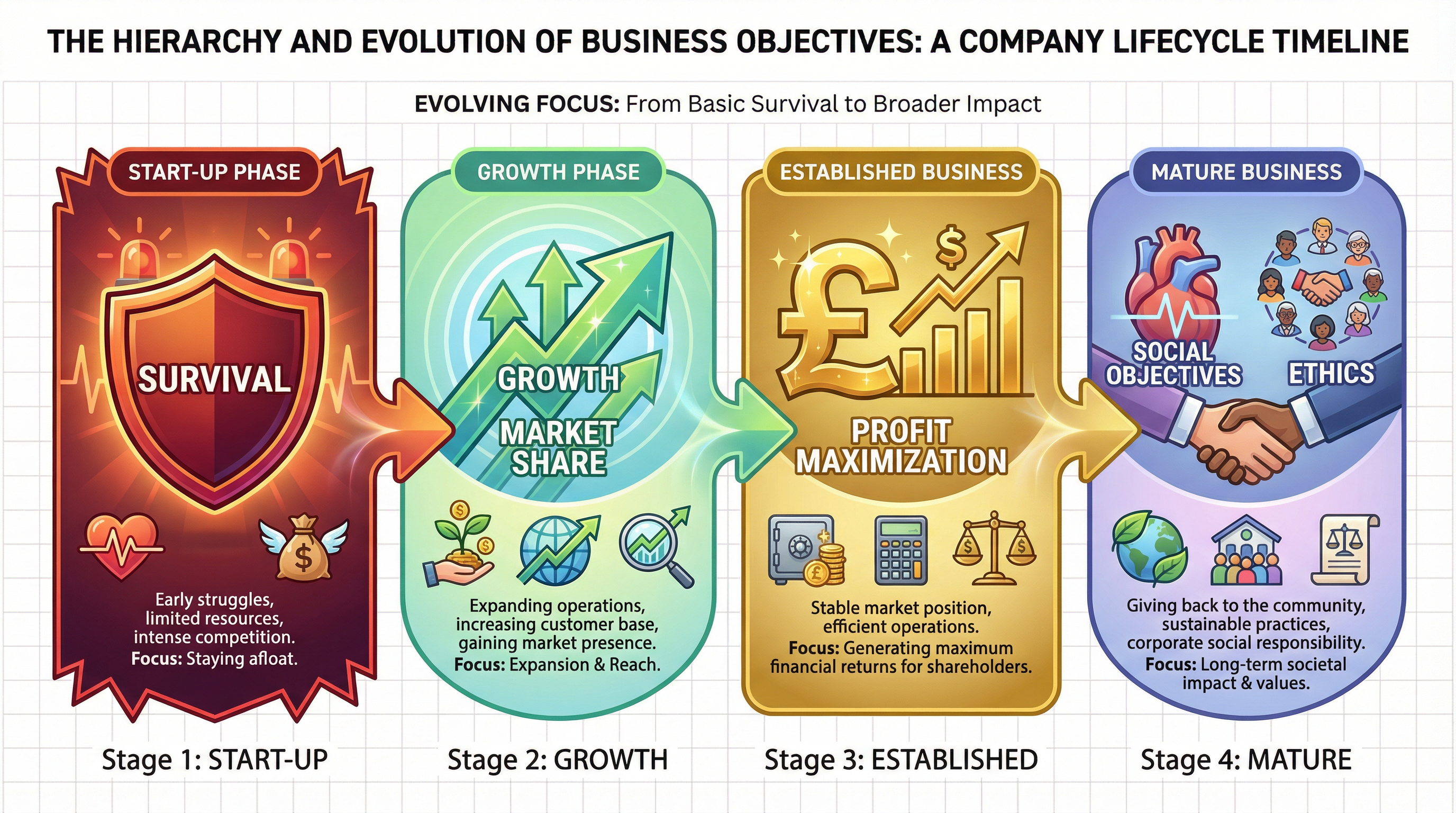

The Dynamic Nature of Business Objectives

Business objectives are not static; they change over time as the business develops and the external environment changes.

- Start-up: The main objective is survival. The business is new, has few customers, and is likely to be making a loss. The owner will be focused on managing cash flow to ensure the business can continue to trade.

- Growth: Once the business is established, the focus may shift to growth. This could involve opening new branches, launching new products, or expanding into new markets. At this stage, profit may be sacrificed for growth, as the business reinvests its earnings.

- Maturity: When the business is mature and has a stable market share, the objective may become profit maximisation. The business will look for ways to increase efficiency and reduce costs to boost profits for its owners/shareholders.

- Decline/Renewal: If a business enters a period of decline, the objective may revert to survival. Alternatively, the business may seek to renew itself by investing in new products or technologies, with the objective of returning to growth.

Stakeholder Conflicts

Different stakeholders have different objectives, and these can often conflict. A key skill is to be able to identify and explain these conflicts.

- Owners vs. Customers: Owners want to maximise profit, which may mean charging high prices. Customers want low prices and high quality.

- Owners vs. Employees: Owners want to minimise costs, which may mean paying low wages. Employees want high wages and good working conditions.

- Owners vs. Government: Owners want to minimise the tax they pay. The government wants to maximise tax revenue to fund public services.

- Owners vs. Community: Owners may want to cut costs by, for example, using cheaper production methods that create pollution. The local community wants the business to protect the environment.