Study Notes

Overview

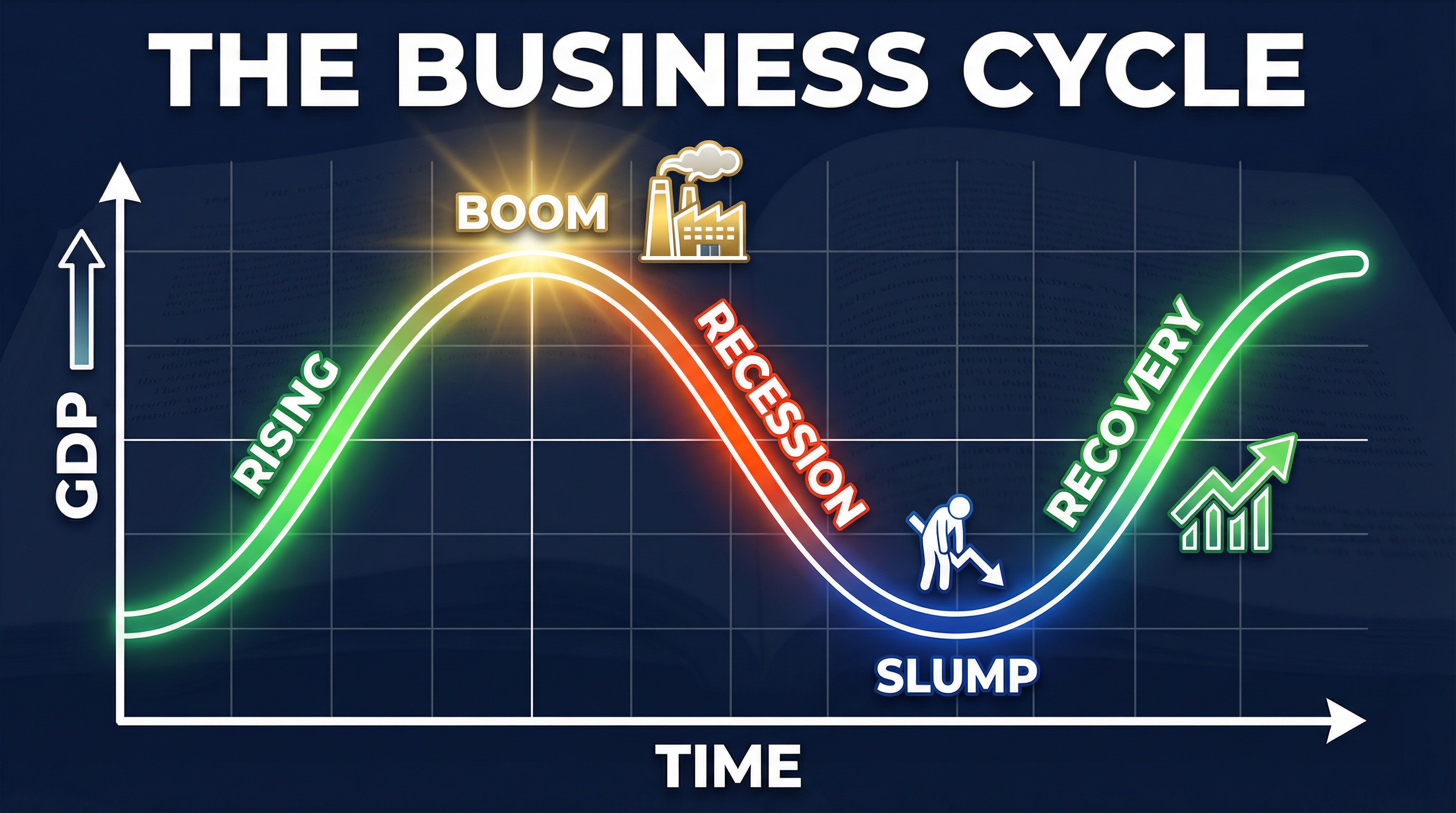

The Business Cycle, also known as the economic cycle, is a core concept in macroeconomics that describes the fluctuations in economic activity over time. For your OCR GCSE Economics exam, it is crucial to understand that these fluctuations are measured by changes in Real Gross Domestic Product (Real GDP). The cycle follows a wave-like pattern, moving through four distinct phases: boom, recession, slump (or trough), and recovery. Examiners expect candidates to not only define these phases accurately but also to analyse their specific impacts on the main macroeconomic objectives: inflation, unemployment, economic growth, and the balance of payments. Furthermore, a high-level response requires an evaluation of the consequences for different economic agents, such as consumers, firms, and the government. This guide will equip you with the detailed knowledge, analytical chains of reasoning, and evaluation skills required to confidently tackle any question on this topic, from short-answer definitions to high-mark evaluation essays. Credit is consistently awarded for using precise terminology, quoting data accurately, and building logical arguments that demonstrate a clear understanding of cause and effect.

The Four Phases of the Business Cycle

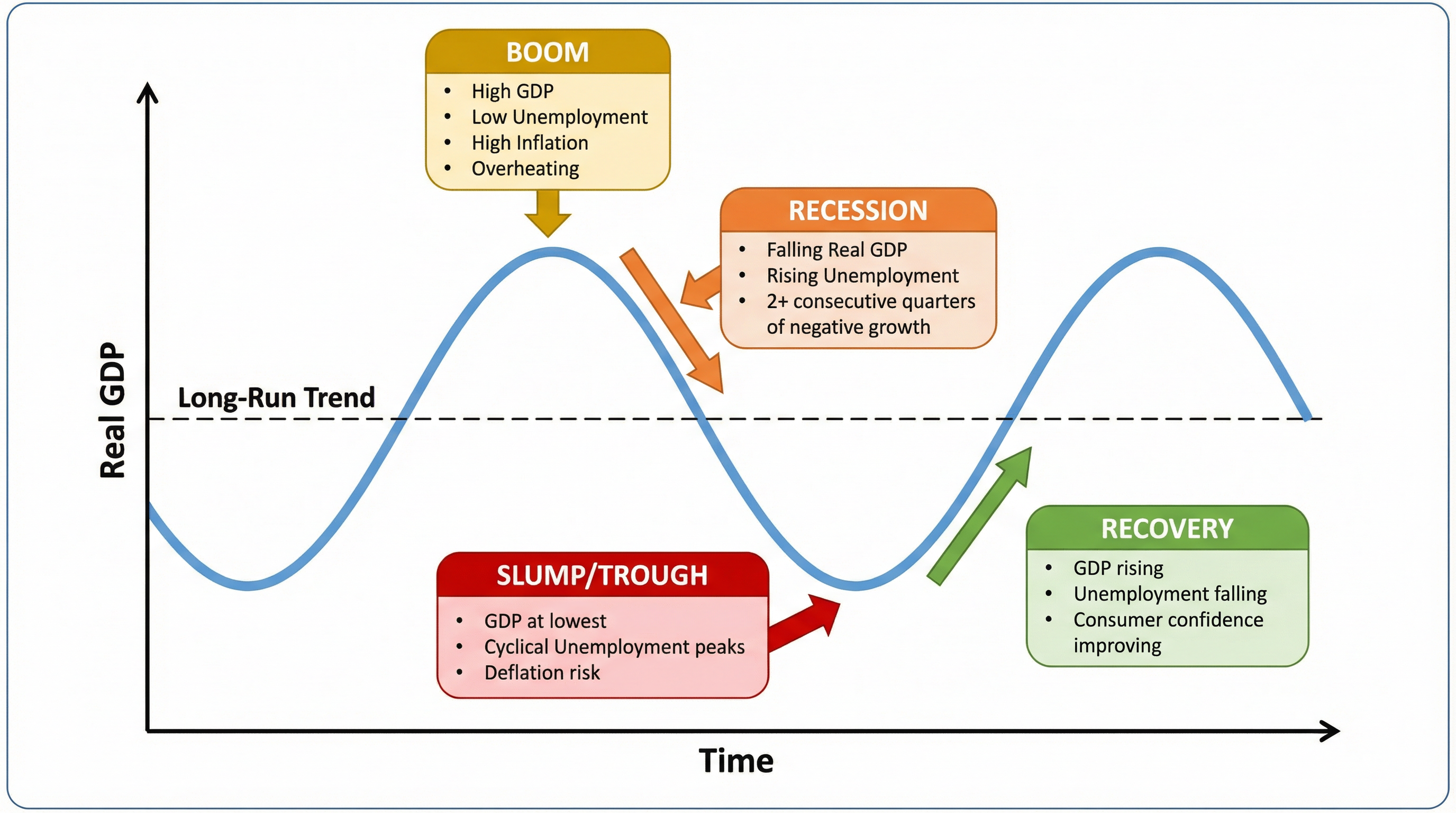

1. Boom

What happens: A boom is the peak of the business cycle. During this phase, the economy is growing at a rate faster than its long-run trend. Real GDP is high, and there is a positive output gap (where actual GDP is above the potential GDP). Consumer and business confidence are very high, leading to increased spending and investment. Firms are operating close to full capacity, and demand for labour is strong, causing unemployment, particularly cyclical unemployment, to fall to very low levels.

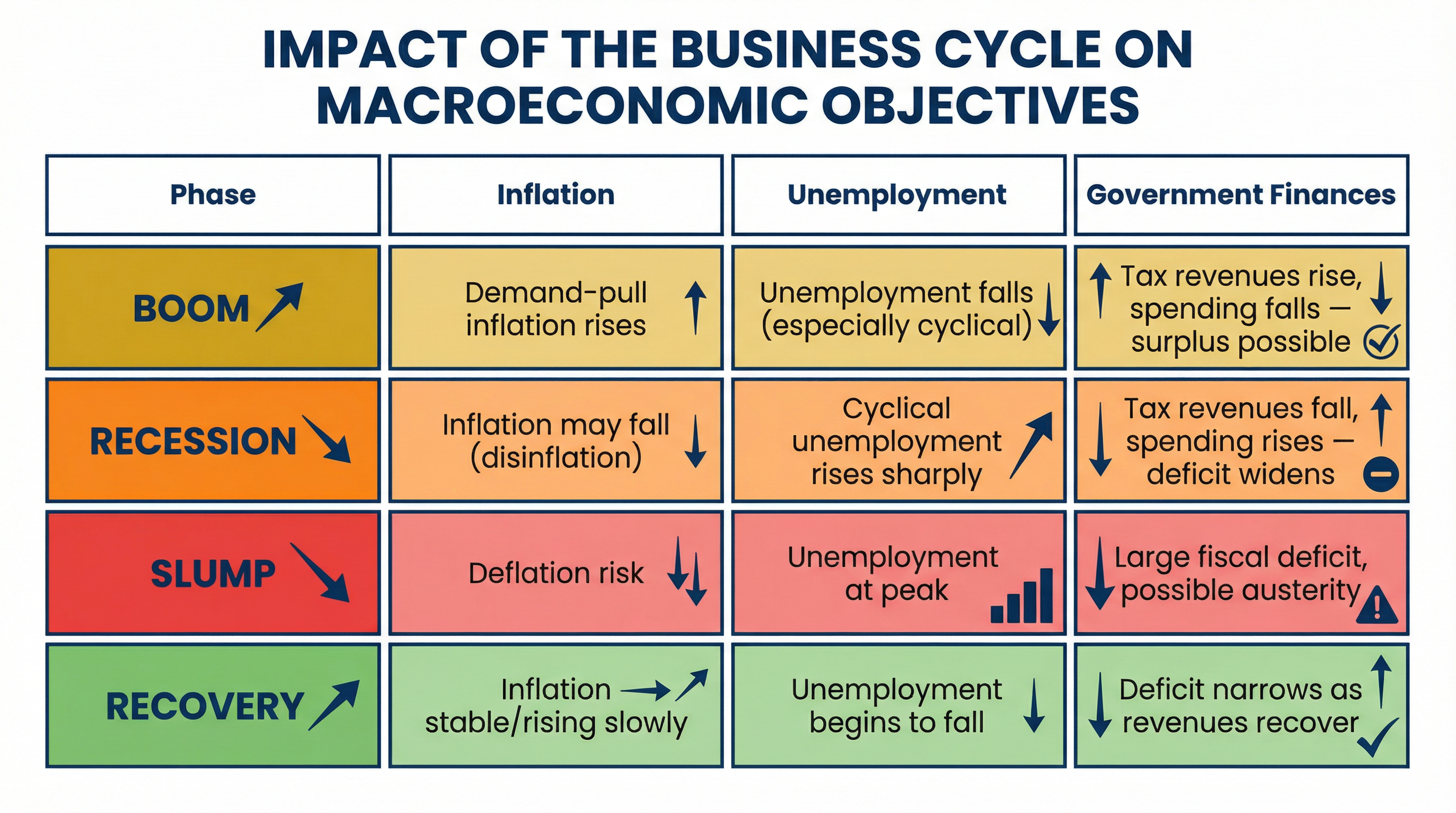

Why it matters: While a boom is associated with prosperity, examiners will reward candidates who can evaluate its downsides. The high level of aggregate demand often leads to demand-pull inflation, as firms raise prices in response to soaring demand. Resources become scarce, and skilled labour shortages can push wages up, further fuelling inflation. There is a risk of the economy "overheating." Additionally, booms can lead to increased inequality and negative environmental impacts due to over-consumption. For the government, tax revenues from income tax, corporation tax, and VAT are high, while spending on unemployment benefits is low, potentially leading to a fiscal surplus (tax revenue > government spending).

Specific Knowledge: Candidates should be able to link a boom to rising asset prices (e.g., houses, stocks) and potential credit bubbles, as seen in the lead-up to the 2008 Global Financial Crisis.

2. Recession

What happened: A recession is formally defined as two consecutive quarters of negative economic growth. This is a critical definition that must be learned verbatim. It means Real GDP is actively falling. A slowdown, where growth is positive but has slowed down, is not a recession, and confusing the two is a common mistake that loses marks. A recession is triggered by a peak in the boom, often followed by a fall in aggregate demand. Consumer and business confidence collapse, leading to reduced spending and investment.

Why it matters: During a recession, the most significant impact is a sharp rise in cyclical unemployment. As firms see demand fall, they cut back on production and lay off workers, creating a negative multiplier effect across the economy. For the government, the fiscal position deteriorates rapidly. Tax revenues plummet as incomes and profits fall, while government spending on automatic stabilisers, like Jobseeker's Allowance, increases. This leads to a widening fiscal deficit (government spending > tax revenue).

Specific Knowledge: The UK experienced a significant recession following the 2008 financial crisis, with Real GDP falling for five consecutive quarters.

3. Slump (Trough)

What happened: A slump, or trough, is the bottom of the business cycle. Real GDP has stopped falling but is at its lowest point. Unemployment is at its peak, and there is a large negative output gap (actual GDP is well below potential GDP). Business and consumer confidence are at rock bottom.

Why it matters: The main danger in a slump is deflation (a sustained fall in the general price level). While falling prices might seem good, they can be very damaging. Consumers may delay purchases, expecting prices to fall further, which reduces aggregate demand and can prolong the slump. Investment is very low as firms have little incentive to expand. The government's fiscal deficit is likely to be at its largest during this phase.

Specific Knowledge: Japan experienced a long period of deflation and economic stagnation from the 1990s, often referred to as the "Lost Decade," which serves as a key case study of the dangers of a prolonged slump.

4. Recovery

What happened: During the recovery phase, the economy starts to grow again. Real GDP begins to rise, and the negative output gap starts to close. This can be kick-started by low interest rates, government intervention (fiscal stimulus), or an increase in export demand. As confidence slowly returns, consumers begin to spend, and firms start to invest in new capital.

Why it matters: As the recovery gathers pace, unemployment begins to fall, and incomes start to rise. Inflation remains low initially but may start to increase as aggregate demand picks up. The government's fiscal position improves as tax revenues rise and spending on benefits falls. The recovery phase sees the economy move back towards its long-run trend rate of growth.

Specific Knowledge: Following the 2008-2009 recession, the UK economy entered a slow and prolonged recovery phase.

Impact on Macroeconomic Objectives

This table summarises the core knowledge you need. Credit is given for explaining why these changes occur.

Podcast Episode: Mastering the Business Cycle

Listen to our 10-minute audio guide to reinforce your learning, with detailed explanations and exam tips.